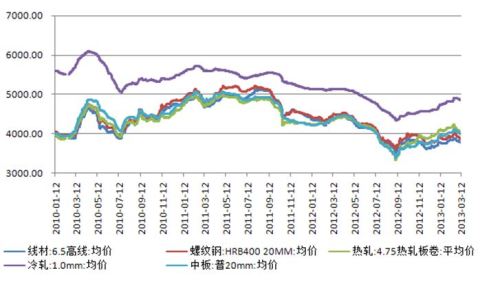

What will happen to the steel market in the future? Take a look at the statistical and analytical data below.

Film disc is one kind of velcro discs, using open sand planting method, planting the specially treated high-performance abrasive on the highly polyester film and carrying out special anti-blocking coating treatment, which can provide uniform grinding effect.

Film disc's advantage is the hidden super coated aluminum oxide corundum. The difference between it and other conventional coatings is that conventional discs have two layers of sanding surface. The outer layer on the sand paper falls down together with the sanding product's dust during sanding, which causing premature clogging.

However, film sanding disc has a hidden anti-clogging coating. This coating makes it last longer than all other traditional sand paper including the best 3M discs. Furthermore, the proprietary film backing causes a very strong bond between the abrasive and the film backing adding to its long life. Finally, the film backing and abrasive is very even, much more than conventional paper, making it much more effective during the entire sanding process.

Film discs are widely used in the grinding of automobile primer, atomic gray, intermediate paint and finish paint. And features: high grinding efficiency, good anti blocking performance, good grinding consisitency without secondary scratch, surface grinding GJ, durable.

Film Velcro Disc,Velcro Grinding Discs,Square Velcro Sanding Pads,Velcro Backed Sanding Discs Henan Yuteng Abrasives Co.,Ltd , https://www.henanyutengabrasives.com

First, the real estate industry carried out a further analysis of the data of the Bureau of Statistics. In December of last year, real estate development and investment amounted to 860.1 billion yuan, an increase of 22.31% and -1.35% respectively over the previous quarter, and an area of ​​40.41 million square meters of land purchased, respectively. Growth of 0.30%, -50.20%; New housing starts for 20153 million square meters, an increase of 35.06%, -18.67%; the increase in the area of ​​commercial housing for sale was 24.89 million square meters, an increase of -13.96%, 72.25%, respectively. The commercial housing sales area was 19.74 million square meters, an increase of 0.74% and 32.72% respectively over the previous quarter, and the completed commercial housing area was 35.10 million square meters, an increase of 0.93% and 219.19% respectively. In addition, the statistics released by the Bureau of Statistics on housing prices in 70 large and medium-sized cities across the country in December last year showed that cities with new home prices rose by 69 and 65, respectively, with the number of cities with a decrease in the chain price and the increase in the number of chain cities.

It can be seen that in December last year, real estate development investment, land purchase, and start of new housing all showed a month-on-month decline, but they still showed different degrees of growth year-on-year; the area of ​​completed commercial housing soared. Although the sales area also increased, the area for sale increased more for sale. The total area has reached 490 million square meters, an increase of 35.2% from the end of the previous year. The overall housing prices remain high, the gains show a slowing trend, and the risks from the inventories in the third and fourth-tier cities are rising.

At the beginning of the new year, the real estate market experienced seasonal cooling and new house transactions continued to slow. According to statistics from the Central China Real Estate Research Department, the number of new houses in 54 major cities in the country fell by 7.3% from the same period in December, compared to 2013. In the same period, it decreased by 15%. However, the land market has been booming, and developers in Beijing, Guangzhou and other places have been grabbing the land. In addition, the national new urbanization plan will come out and the construction of urban agglomerations will accelerate. In the future, the middle reaches of the Yangtze River, the Central Plains urban agglomeration, the Shandong Peninsula, and the Chengyu City Cluster will be fostered by the country.

In the short term, the real estate market differentiation will continue to intensify. First-tier cities will find it harder to reduce housing prices. Real estate starts and construction in January and February will remain in a state of “off-seasonsâ€; in the medium term, the central bank continues to de-leverage, the US reduces QE, and so on. Will be reflected in the real estate market; long-term, new urbanization will inject the follow-up development momentum for the real estate market. This year, the real estate market is operating with “stabilization†as its main focus, and the total demand for related building materials may have weakened compared to the same period last year.

II. Infrastructure Construction According to the latest statistics from the Bureau of Statistics, in the month of December of last year, investment in urban fixed assets increased by 17.2% and 14.2% respectively year-on-month. Cumulatively, the total planned investment growth rate of new projects started to fall by 0.1 percentage point, the total project investment growth rate of construction projects fell by 1.7 percentage points, and the investment growth rate of investment funds dropped by 0.1 percentage points. Since December last year, due to the off-season construction and construction, and the tightening of market funds, related investment in the infrastructure sector has continued to slow. In the short-term, seasonal negative factors still dominate, coupled with the impact of the Spring Festival holidays, the related investment continues to be weak.

Looking at the whole year of last year, the growth rate of fixed asset investment remained stable and slightly weakened. Recently, local ** was held in an intensive manner, and the target of reducing GDP and investment growth became mainstream. There were 20 out of the 26 provinces that had held “**â€. This year's GDP growth forecast is lowered. The local government work report involves three aspects: “reducing the fixed investment targetâ€, “controlling debt riskâ€, and “resolving excess production capacity.†This may imply that the local investment competition will be closed. The country will be determined to solve the problem of local debt and excess capacity. However, when economic growth once again touched the country's "bottom line", "investment" does not rule out again as the main force of "steady growth."

From the perspective of investment plans launched in the New Year, this year, the construction of highways, rails, and other transportation infrastructure will continue to focus on investment in all areas. Investment in road construction will be tilted toward rural areas or underdeveloped areas, and the focus of urban transportation infrastructure will be shifted to public transportation. Traffic is the focus of development; the Ministry of Water Resources will focus on the development of people’s livelihoods and water conservancy and safeguarding national water security. It will start the implementation of a number of major water conservancy projects; the state railways will arrange 610 billion yuan in investment in fixed assets and put more than 6,600 kilometers of new lines into operation. It is expected that the growth of infrastructure investment will continue to weaken during the whole year, and the total investment may decline, but there is limited room for decline.

From the above analysis, in the short term, real estate and infrastructure construction will continue to shrink as the “off-season†dominates. For manufacturing, January and February are still the traditional off-season for construction machinery, household appliances, and shipbuilding industries, and their demand will remain weak. From a year-round perspective, real estate and infrastructure investment are not optimistic. The growth rate tends to be weak, and the total investment volume may also decline slightly. The manufacturing sector may maintain a weak recovery, and “decapacity†and “structure adjustment†will further accelerate.

It seems that the future steel market is still not optimistic.